The Scam Machine: How India Is Losing ₹50 Crore a Day

India is losing ₹50 crore every single day to cyber scams, even as over 7,000 new complaints pour in daily—numbers that reveal a digital crime wave far beyond anything the country has faced before. Behind this relentless surge is a highly organised global network that targets ordinary people with alarming precision. This article uncovers how online scammers outrun the system and win.

It was a usual busy morning at the State Bank of India (SBI) Perinthalmanna branch in Malappuram district when Rajan (name changed), a man in his early seventies walked in and requested the officials to close his fixed deposit of ₹60 lakh. He asked the clerk to transfer the amount to a particular account number. Sensing something unusual, the clerk notified the branch manager, who asked Rajan why he wanted to do this.

Rajan said he had invested in a trading app and had deposited ₹40,000, for which he had received a return of ₹90,000. He showed the app’s dashboard to the manager, displaying a graphic image of his investment and the supposed doubled returns. But on checking, the manager found that no such amount had been credited to Rajan’s account.

The manager tried to explain that this was a scam and that the account number he had provided was linked to fraud, even showing Google reviews that confirmed it. But Rajan refused to listen. The manager sent him back that day, telling him the net banking services were down.

The following day, Rajan returned with another set of account numbers, which he said “were real accounts.” The manager then contacted his daughter—a doctor working in another state—who finally dissuaded him from falling into the trap.

“He still holds a grudge towards SBI for having stopped him from becoming rich” Girish C, Chief Manager (Operations) in the Regional Business Office of SBI, told OBC.

Girish is one among the thousands of bank professionals dealing with victims—and potential victims—of online financial scams on an every day basis. With cyber-financial fraud surging nationwide, officers like him now spend much of their time trying to stop people before they get trapped.

The Trouble with Numbers

The scale of suffering faced by victims of online financial fraud may not be fully captured in numbers. But looking at how poorly the state is faring can at least help in planning better corrective measures.

According to the Indian Cyber Crime Coordination Centre (I4C), an initiative of the Ministry of Home Affairs to deal with cybercrime in the country, Indian victims report losses of around ₹50 crore every single day. Of this, 35% of reported amounts are more than ₹50 lakh. On average, more than 7,000 cybercrime complaints are registered per day (as of May 2024). Between January and June 2024, ₹11,269.83 crore was reported to be involved in online financial fraud across 8,50,034 complaints. Of these, 24,415 complaints remained unattended as of July 15, 2024.

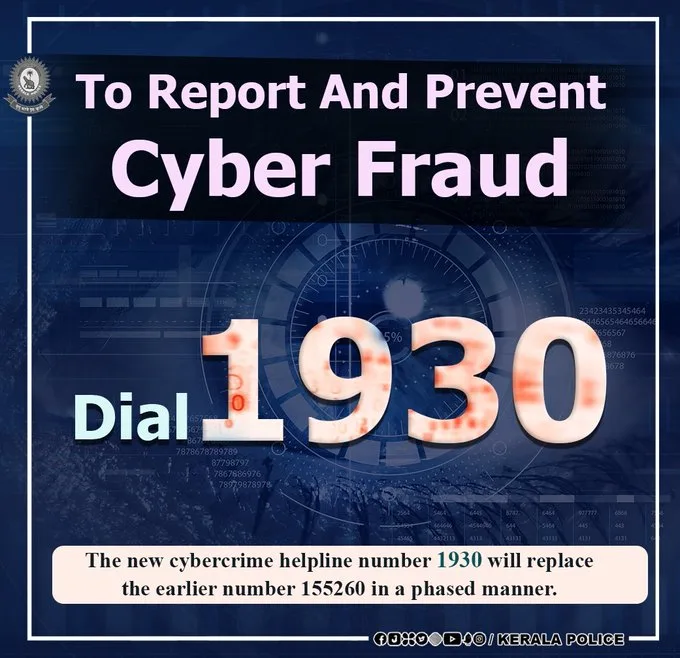

The national helpline 1930, which allows citizens across all states and UTs to report cyber-financial fraud, now receives around 60,000 calls every day.

The Ministry of Home Affairs, in an answer to an unstarred question in Lok Sabha, said that more than 23.39 lakh cyber complaints had been reported as on March 11, 2025. It also states that over ₹4,386 crore has been saved in more than 13.36 lakh complaints reported through 1930 and the National Cyber Crime Reporting Portal (NCRP) since its inception.

Counting the Losses

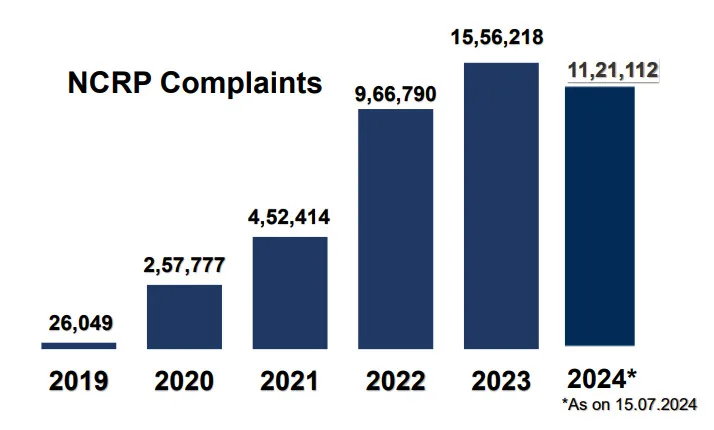

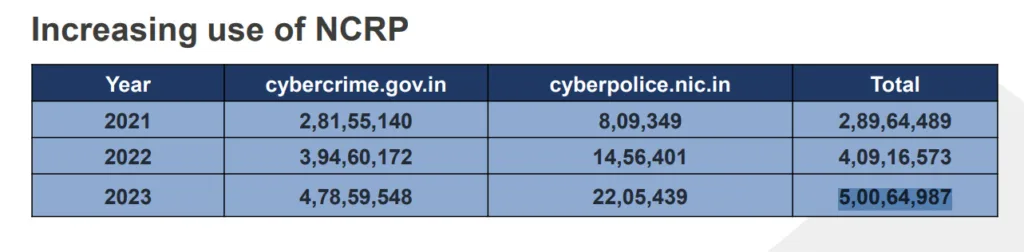

An exponential growth can be seen in cybercrime trends from NCRP data, where from 2021 to 2022 an alarming 113.7% increase was reported. From 2022 to 2023, this figure stood at 60.9%.

Data from the NCRP and the United Nations Office on Drugs and Crime (UNODC) shows that the major modus operandi behind online financial scams in Southeast Asia includes illegal stock-market schemes, fraudulent investment platforms, fake gaming apps and digital-arrest scams.

“Investment scams are usually reported very late because victims realise the fraud only after losing a substantial amount of money. They start with small investments and receive initial returns. When they invest more and attempt to withdraw, they’re told to pay extra charges—sometimes taxes—to release the returns. By then, they may have already lost a huge amount. And then the scammers disappear. Recovery rates in these cases are extremely low because the money is often converted into cryptocurrency by the time victims report it, it’s far too late,” explains Hari Sankar IPS, DIG of Thrissur Range and former Superintendent of Police (Cyber Operations) with the Kerala Police.

While talking to OBC, he recounted one case where the police managed to return ₹70 lakh to a victim who had lost ₹1 crore to an online scam. Digital-arrest cases, he says, show better recovery rates because victims realise what’s happening much faster and report immediately. “If the money is still somewhere in the banking chain, we can block it and return it to the victim,” the officer explains.

Hari Sankar explains that these fraudsters operate vast networks outside India. Using large webs of fake social-media accounts, they identify affluent users, befriend them, and lure them into investing. They also have agents here who create ‘mule accounts’—bank accounts taken on rent—for victims to deposit money into, earning commissions in return.

Girish C echoes the same concern. “The fraudsters offer commissions of around ₹5,000, which is huge for many students. Some students in Kerala have even been arrested by police in other states for having such accounts in their names. They don’t realise the danger they’re stepping into.”

“When a student’s account—usually with no income—suddenly receives large deposits, the bank gets alerted and we freeze the account. Banks can’t recover this money, so we file a complaint with the cyber cell,” Girish says.

The I4C reports that nearly 4,000 mule accounts are being flagged in India every single day as of July 2024.

Operation Cy Hunt, a statewide cybercrime crackdown by the Kerala Police, was launched in late October 2025 to create a deterrence against mule accounts. A press note from the Kerala Police dated 30.10.2025 says that 382 cases were registered and 263 suspects were arrested in its first phase as part of the statewide raid under the operation. “The operation will soon be launched at a national level to coordinate similar actions across all states,” says the DIG.

The Roadblocks Ahead

Sidharth Kulangara Thodiyil, a cyber expert who previously worked with the Kerala Police Cyberdome, says he receives more than 10 enquiries every day about money lost in such financial scams. Since these involve financial fraud, the police register them as civil cases. “We all know the tedious journey of going through a court case. Most of the time, victims get dissuaded because the process wears them out. A fast-operating mechanism is barely in place,” Sidharth says.

“Almost all laws relating to cybercrimes in India are bailable. Even if they’re caught, the punishment doesn’t amount to much. If they scam 100 people, they usually end up repaying only what was taken from 10. That’s why these networks find India a ripe place to do business,” he adds.

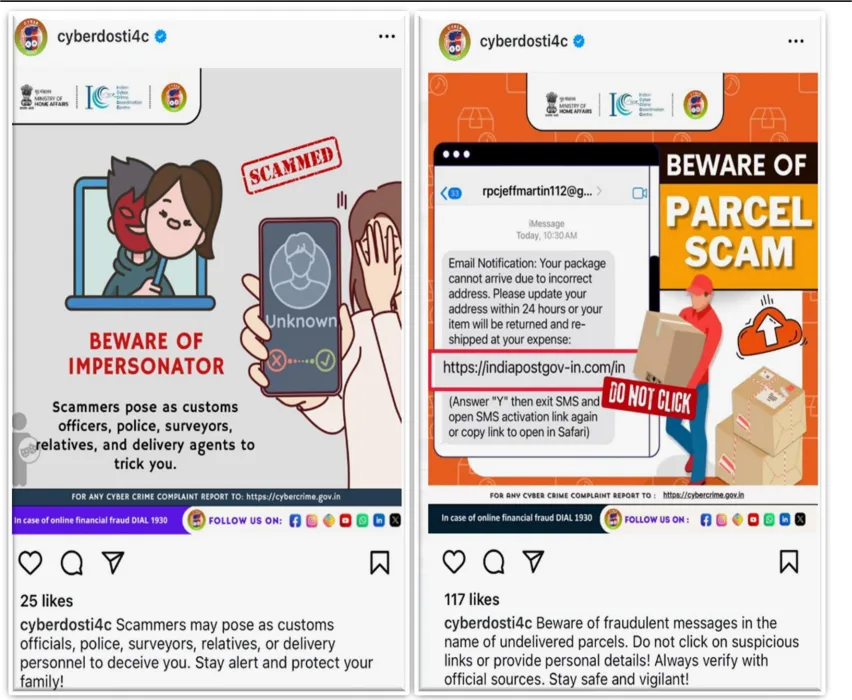

In cases of digital arrests, scammers use call spoofing to contact victims, posing as officials from agencies such as the CBI, RBI, NIA, ED, Narcotics Control, banks, and others. The vulnerable population—especially senior citizens—often fails to spot the fallacies in these impersonation acts.

The channels through which money exits include cryptocurrency, ATM withdrawals, hawala networks, international fund transfers, and even physical gold. Hence, retrieving the money becomes a herculean task.

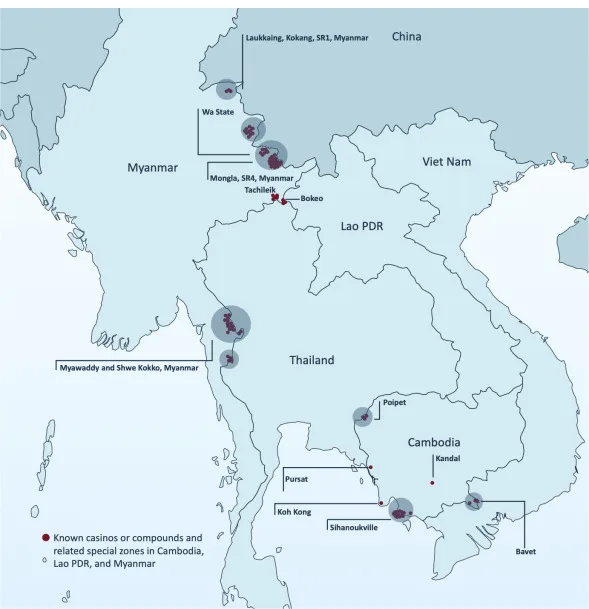

The criminal infrastructure runs through digital advertisements, mule accounts, SMS, WhatsApp groups and numbers. Sidharth, who has helped people from Kerala who were trapped in scam centres in countries like Cambodia and later escaped, says these networks grow massive and decentralised, holding personal data of potential victims worth millions.

A Few Bright Spots

Hari Sankar notes that Kerala was the first state to formally submit recommendations to the RBI Governor and the Ministry of Home Affairs in March 2024, after cyber scamsters operating from various countries had swindled more than ₹200 crore from the state the previous year. The move was initiated by then Kerala DGP Shaik Darvesh Saheb.

Shaik Darvesh Saheb has also proposed creating credibility scores for every bank account based on defined parameters. When a user attempts a transaction with an account that carries a low credibility score, a pop-up alert should warn them about the potential risk. If implemented, this could bring cyber-financial fraud down to almost zero. Hari Sankar says that employing such a method would allow banks to break this cycle once and for all.

The rate of citizen and police engagement with the NCRP also presents a silver lining. Engagement with the NCRP grew from 2,89,64,489 in 2021 to 5,00,64,987 in 2023. The Citizen Financial Cyber Fraud Reporting and Management System claims to have benefited around 7.5 lakh victims by saving ₹2,572.91 crore as on July 22, 2024. Police have repeatedly stressed that reaching out to 1930 within two hours of losing money significantly increases the chances of recovery.

Awareness can go a long way. Government campaigns have reduced the numbers, but a section of the population—especially senior citizens—remains outside these social-media efforts and must be reached, Hari Sankar notes.

The task of building awareness, enabling prevention, taking corrective action, and enforcing legal crackdowns cannot rest on a single entity. It requires coordinated action from civil society, the government, police, banks, and other key stakeholders. The most crucial need is a strong and transparent citizen-reporting system. The NCRP claims to have begun this work, but public awareness on how to use it still has a long way to go.