India’s Fuel Price Excuse Kit Needs an Update: Oil Bonds Are No Longer An Excuse

For years, oil bonds have been invoked as the convenient explanation for India’s stubbornly high fuel prices, but with the final repayments now completed, the numbers reveal a different story;oil bond liabilities were only a small fraction of the massive revenues the government earned from fuel taxation.

For over a decade, Indian consumers have watched a familiar ritual unfolding-when global crude oil prices rise, petrol and diesel prices in India climb almost instantly in the name of ‘international market pressures’. But when crude oil prices crash, retail fuel prices discover the virtue of patience, restraint and fiscal discipline. During the 2014-2020 period when global crude oil prices saw repeated declines-including dramatic pandemic era collapse-the Centre raised excise duties multiple times instead of +proportionately reducing pump prices, leading to record-high fuel tax collections.

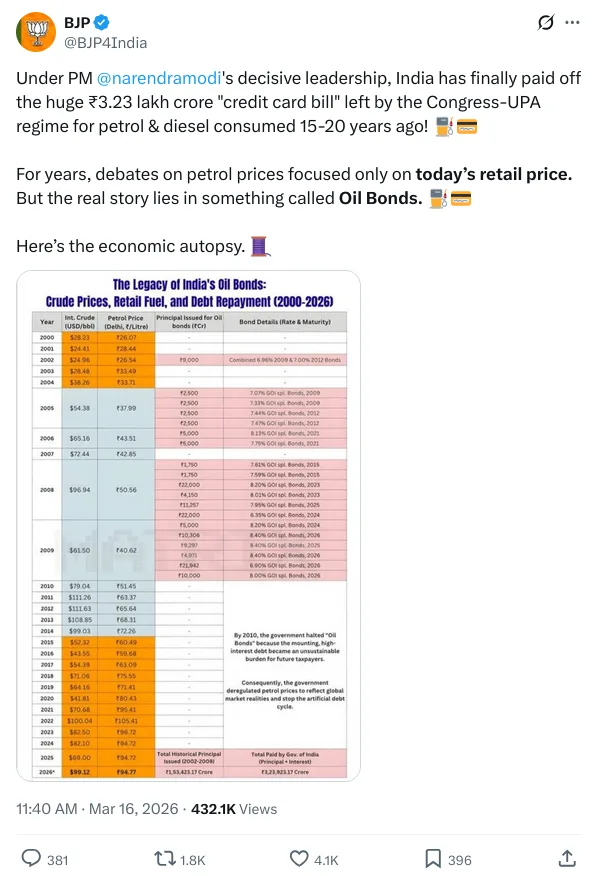

The Government frequently blamed the UPA-era ‘oil bonds’ as the inherited burden preventing deeper cuts, with Finance Minister Nirmala Sitharaman arguing (in 2021) that the Centre was still servicing liabilities created by previous governments. Since then the oil bond argument has resurfaced with consistency- dusted off whenever fuel prices become politically inconvenient. Even after more than a decade of BJP rule at the Centre, the right-wing social media had begun reviving the oil bond narrative as early as March itself almost as though the groundwork was being laid well in advance for the inevitable fuel price hike.

In March 2026, the Government of India repaid the final interest instalment on the oil bonds and cleared the debt. Soon after, the verified official Bharatiya Janata Party (BJP) social media accounts and other influential right-wing accounts coordinatedly shared copy-paste posts across multiple social media platforms, emphasising the alleged financial stress the oil bonds placed on the NDA government.

What are oil bonds

Oil bonds were conceptualised and first issued in April 2002 by the Bharatiya Janata Party (BJP)-led National Democratic Alliance (NDA) government, under the leadership of late Atal Bihari Vajpayee.

Between 2005 and 2010,the UPA Government primarily issued oil bonds to shield consumers from the impact of ricing global crude oil prices. These bonds carried interest obligations and were designed to be repaid over time.Following the end of the UPA regime, the NDA government continued servicing the interest payments and repaying the bonds in phases.

The actual oil bond burden

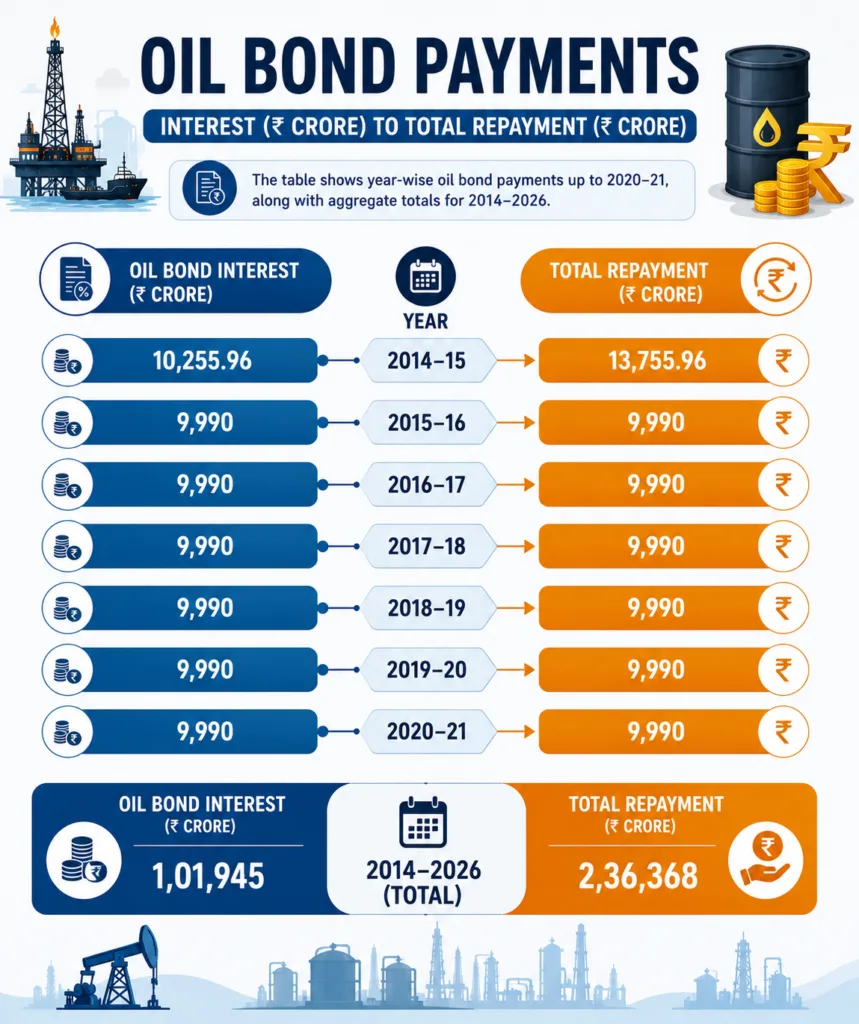

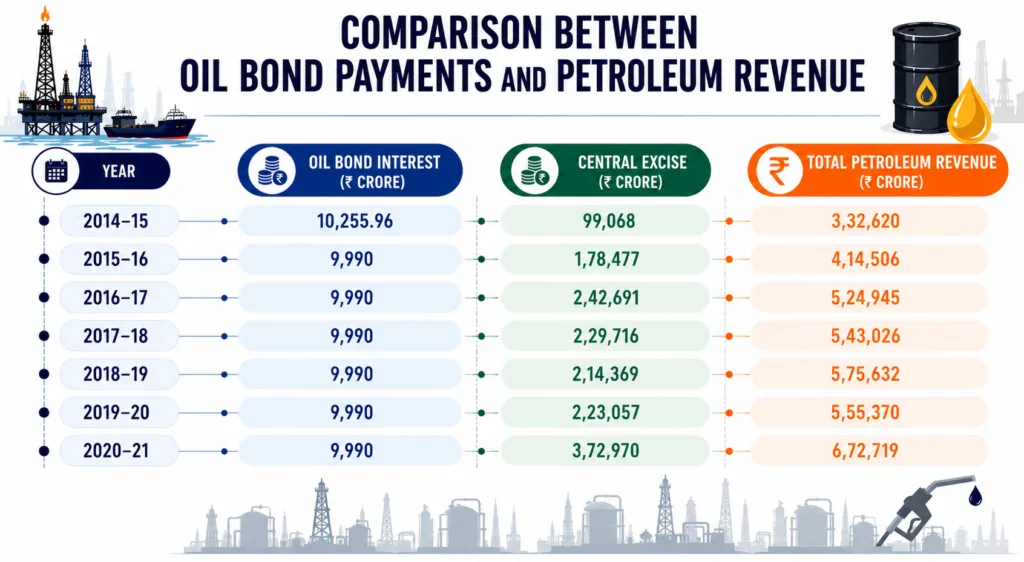

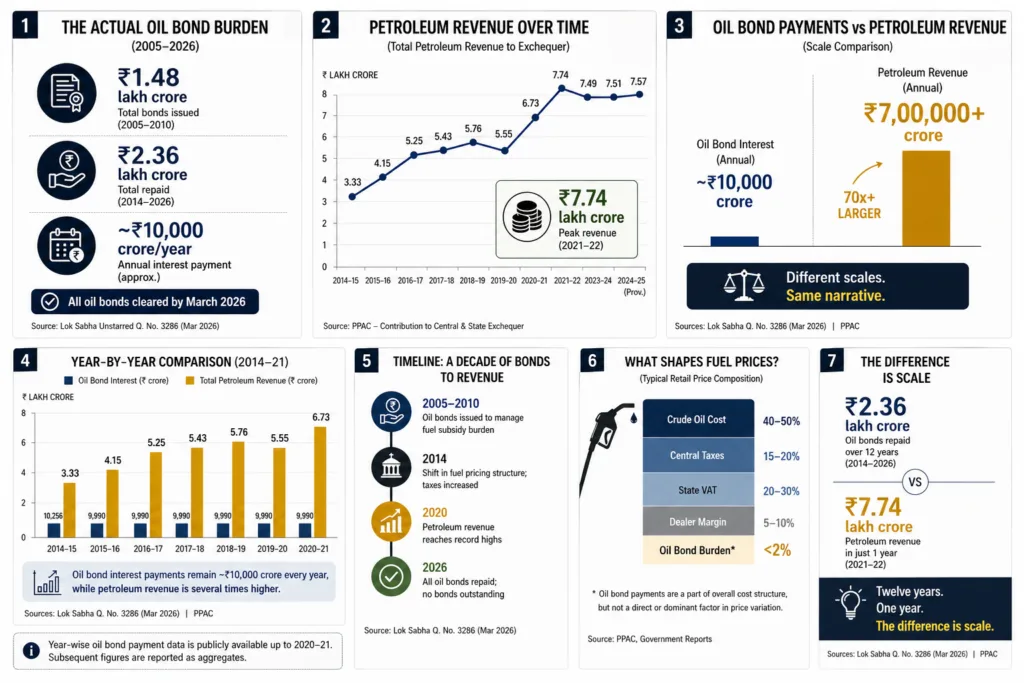

Oil bonds issued between 2005 and 2010 amounted to over ₹1.48 lakh crore. After 2014, repayments continued in phases. For several years, annual interest payments stayed close to ₹10,000 crore. Total repayment between 2014 and 2026, including principal and interest, stood at ₹2.36 lakh crore approximately.

What does the government earn from fuel?

To assess the impact, we compared annual interest payments with the government’s fuel earnings, providing clarity.

Over the same period, revenue from petroleum has remained consistently high. Central excise collections alone exceeded several lakh crore each year, rising sharply after 2014 and peaking in the years that followed. When state taxes are added, the total contribution from petroleum to the exchequer reaches several lakh crore annually.

In some years, this number crosses ₹7 lakh crore. Against this, oil bond interest payments remain a small, fixed outflow.

Year-wise oil bond payment data is publicly available up to 2020–21. Subsequent figures are reported as aggregates.

What shapes fuel prices?

Fuel prices are not determined by any single factor. They are shaped by a combination of factors-global crude oil prices, central excise duties, state taxes ,dealer margins and currency fluctuations. Oil bond payments exist within this large framework as part of the government’s broader fiscal obligations,but they do not operate as a direct or dominant trigger for day-to-day fuel price revisions. At best they form part of the long term financial backdrop against which taxation and pricing decisions are made. Therefore, attributing fuel price hike solely to the interest burden of oil bonds is both misleading and overtly simplistic especially when a broader analysis of fuel taxation,crude price trends and government revenue patterns over the years tells a far more complex story. After all, it has been well over a decade-perhaps it is finally time to retire oil bonds from India’s endlessly reusable fuel-price excuse kit.

Sujith A

Open Source Intelligence Researcher and Mis/Disinformation tracker. Passionate about investigations and a big fan of Sherlock Holmes.

View all posts by Sujith A